Originally published on March 27, 2023, updated March 4, 2025

Menu

Join Our Email List

- Receive our monthly newsletter.

- Stay up to date on Amazon policies.

- Get tips to grow your business.

/%5BeComEngine%5DLogo-2019-linear.svg "eComEngine Logo")

| Review Monitoring Quickly identify review trends |

| Review Monitoring Quickly identify review trends |

The early years of eCommerce were all about marketing, advertising, and making a sale. In the last couple of years, business owners’ focus broadened to include operations as they saw colleagues exit with high multiples as a result of the high level of aggregator buying activity. Top-line revenue quickly took a backseat to profitability.

Focusing on profitability means you have many more levers to control. It's easy to get confused about what is driving performance.

That's where Amazon business planning comes in. One of my favorite ways to ensure all levers are being managed appropriately is to predict or design the future. Stephen Covey said it best with Habit 2 in his book Seven Habits of Highly Effective People, "Begin with the end in mind." That doesn't just apply to a vision board, it applies to your numbers as well.

But before we get to the numbers themselves, the plan should start with utilizing your imagination and creativity. As an entrepreneur, you probably have these thoughts all the time. But now we're going to put some rigor behind them. Take a few minutes and think about your biggest opportunities for the year. This may include:

Jot down your top three; these goals will be the drivers for your yearly forecast.

On to the fun part, at least for those of us that love numbers! Let's determine how each scenario impacts you financially.

For each opportunity, think about how much it will add to your revenue and what it will cost you. I like to do this on a monthly basis because it allows me to see the timing involved. I can show when the cash is going to be spent and when I will start to receive revenue.

Typically, there are some upfront costs before you start to reap the rewards. By looking at the scenario in monthly terms, you can understand the impact on your cash. This is important because the scenario may generate a lot of income, but if you don't have the cash to launch it, your entire business could be in jeopardy.

Develop a tab in a spreadsheet for each of your three scenarios. This will allow you to isolate your activities and start to understand their priorities. Focus on the "low-hanging fruit" first and ensure that you don't get overwhelmed by doing too much. You can manipulate your scenarios easily with less confusion if you isolate them. Once you have these new initiatives mapped out, you are ready to apply them to your baseline data.

The previous year's financial information is your baseline data. You will set up a tab in your spreadsheet for baseline data and pull your Profit and Loss from your accounting system as an Excel file and copy it into this tab. Then, look at each line of activity and apply an adjustment. In general, will revenue stay the same or will it slightly increase? Is a product going to be discontinued, signaling a drop in income?

Ask the same sort of questions about your expenses. Were any expenses a one-time thing? Will your vendors be increasing their pricing on your standard products? Are there any rent increases on the horizon?

I like to call this exercise "considering your changes to maintain your operations." What will stay consistent and what will change? (Note: don't add in your three initiatives for the year just yet; this is just about taking a look back and asking yourself if this were a standard year, what would need to be adjusted to "repeat" that performance?)

Related reading: Leveraging the After Action Review Process for eCommerce

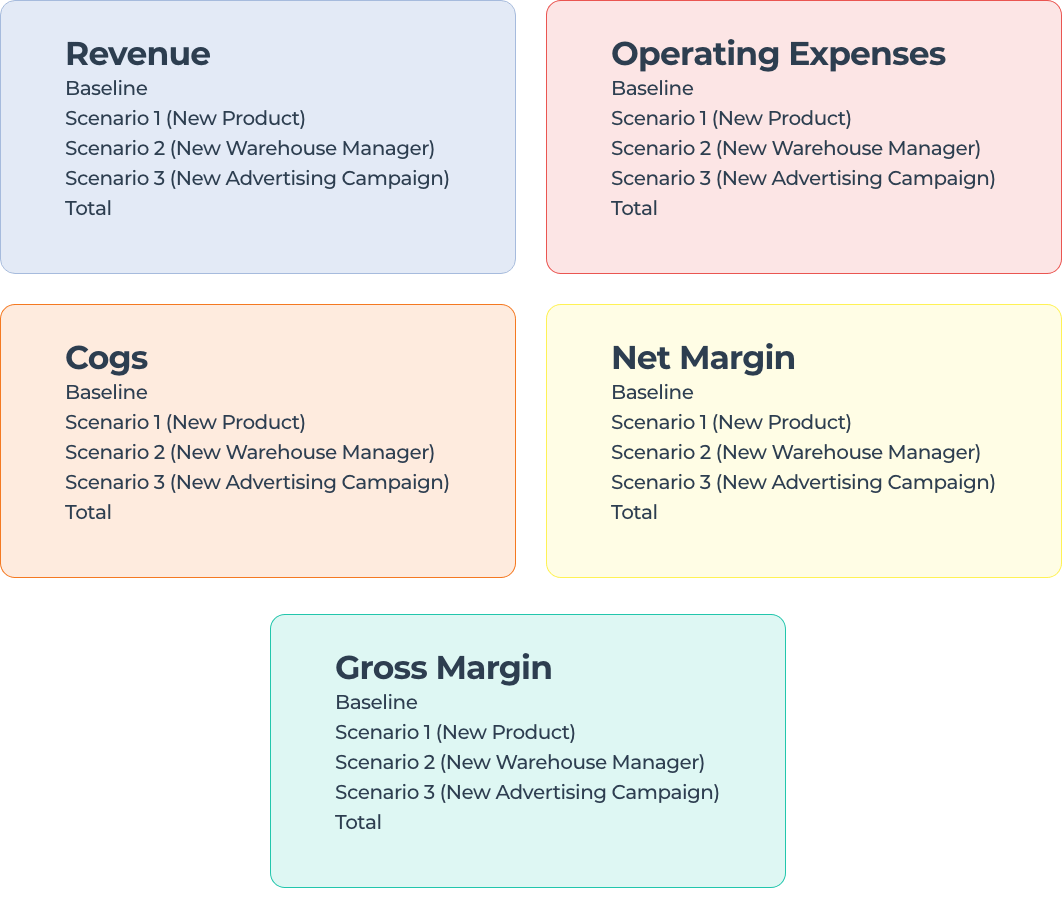

Now you are ready to start looking at the baseline data with the new projections. I suggest creating a summary tab where you're just pulling the totals in to see your baseline revenue, cost of goods sold (COGS), gross margin, operating expenses, and net margin. Your summary spreadsheet will be set up with the information below.

Once you have gathered this information, you can begin to track your performance during the year against these activities. This can be a challenge with spreadsheets. There are some forecasting tools available that integrate with your accounting system. Your accounting professional may be able to recommend one.

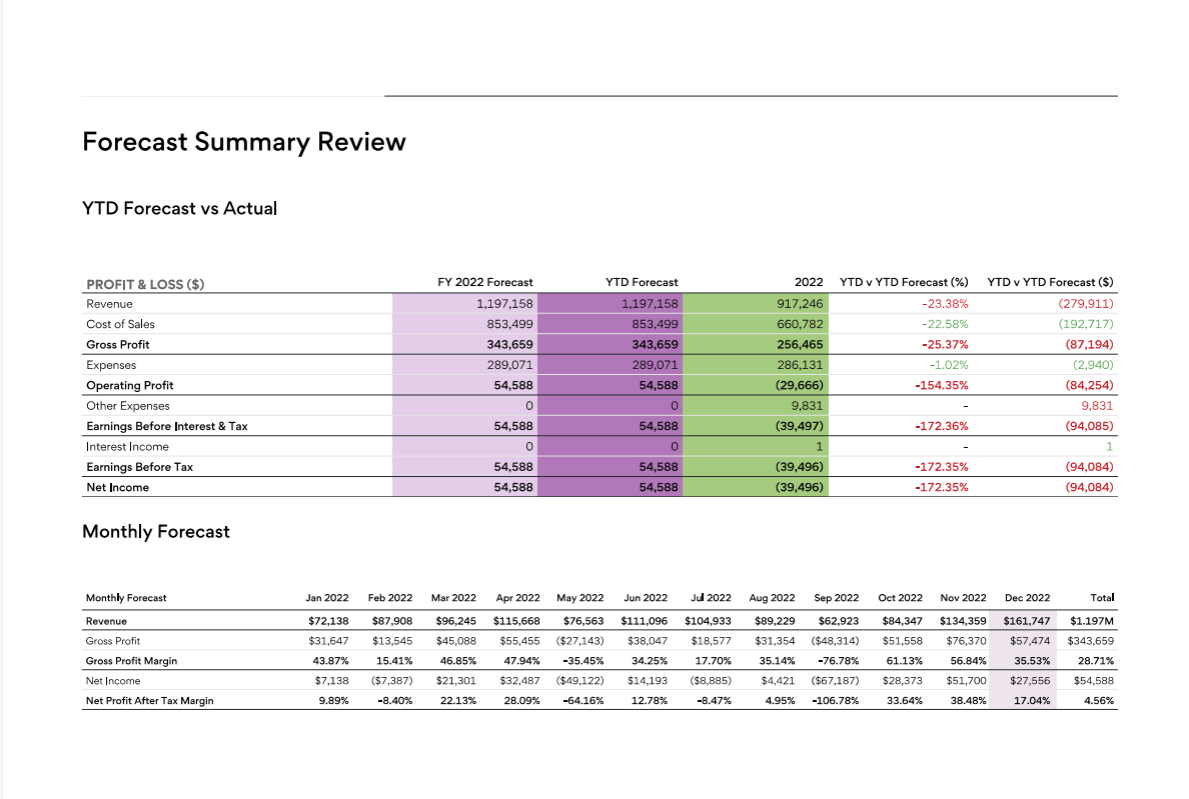

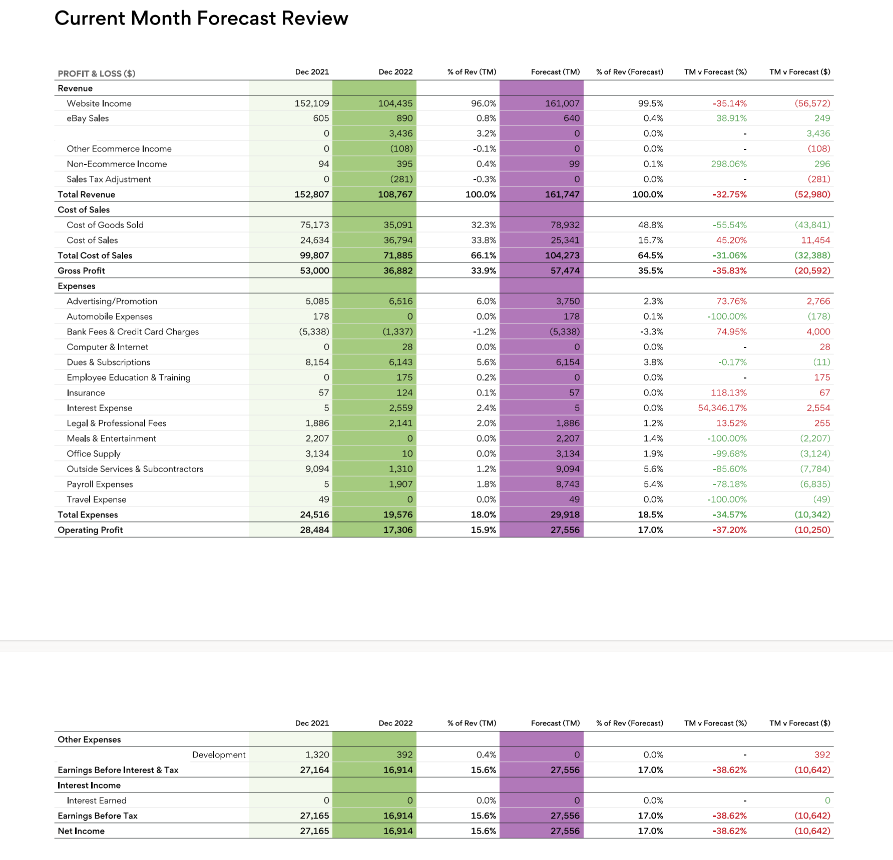

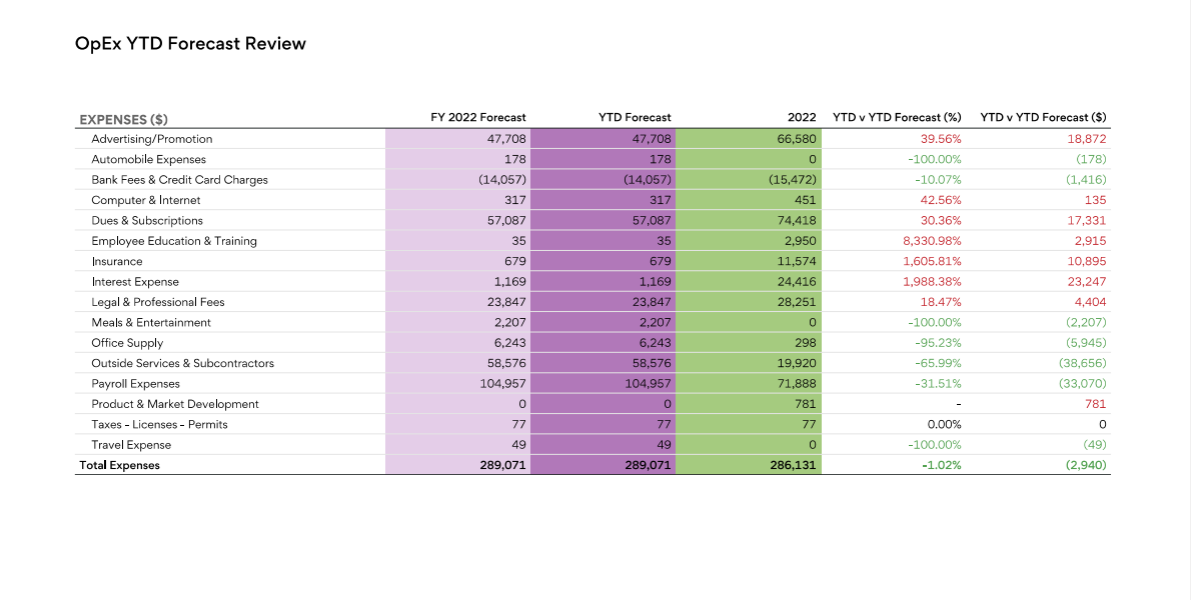

At bookskeep, we use and love a tool called Fathom. It allows us to forecast and monitor our client's progress and generate graphical reports that help us spot business trends.

You can see a couple of the pages we produce below.

If you're just getting started with your Amazon business planning, a spreadsheet will take you a long way down the road. The thought processes and monitoring/adjusting are the most important pieces. These things allow you to take the data from your business performance and use it to make good operational decisions.

If you're just getting started with your Amazon business planning, a spreadsheet will take you a long way down the road. The thought processes and monitoring/adjusting are the most important pieces. These things allow you to take the data from your business performance and use it to make good operational decisions.

As your business grows and gets more complicated, the software's forecasting and reporting tools will help you continue this important activity without spending multiple hours lost in spreadsheets.

We advise our clients to set that money aside in a bank account as if they were paying themselves. When the day arrives that you strike out on your own, you have some salary set aside to act as a buffer, should you have a lean month.

The business would have been setting this money aside routinely, so you can act confidently and not from a place of fear. You will learn to follow this model repeatedly and set aside the payroll funds before you bring on a new employee. When you hire, you have a buffer for them to help offset the training costs and the ramp-up to productivity.

The business would have been setting this money aside routinely, so you can act confidently and not from a place of fear. You will learn to follow this model repeatedly and set aside the payroll funds before you bring on a new employee. When you hire, you have a buffer for them to help offset the training costs and the ramp-up to productivity.

There are many factors to consider before you begin to expand your product line. One, of course, is being able to afford the launch of that product.

From a financial perspective, I suggest that you begin planning for that next product right away. If you are selling your first product at a good gross margin (usually around 30% or more) and you are keeping your advertising and other operating expenses in check, then you should have cash to set aside for product development.

The Profit First cash flow strategy can be expanded upon to ensure that you’re planning for growth in your business and able to expand your brand appropriately.

Some of our Profit First clients plan to fund the next product by setting aside more inventory funds than are needed to simply replenish their existing product. They add 10-15% above the replenishment rates to grow the inventory bank account so that funds are available when they are ready to begin the development of their new product.

This strategy can work well if you keep track of those dollars and the growing amount you are earmarking for this purpose with each allocation. You can do this with a simple spreadsheet.

This strategy can work well if you keep track of those dollars and the growing amount you are earmarking for this purpose with each allocation. You can do this with a simple spreadsheet.

One downside to this type of approach is that it's easy to watch that bank balance grow and then when another use comes up, you reach into that account for the funds. In a flash, that money is spent. Only later do you realize that you did not reserve the funds as originally planned.

One common trap is inadvertently funding increased inventory buys of your existing products because of expected future demand for your busy season. It's great to set aside an additional percentage for sales growth, but just be clear that is a separate strategy from the funds you are earmarking for a new product.

A simple strategy that we recommend to clients to resolve this issue is to create a Product Development bank account. It can be a savings or a checking account. After you allocate to inventory in the typical Profit First manner, you'll then allocate to your profit, owner pay, taxes, operating expenses, and product development bank accounts

You can do a profit assessment on your business and then follow those percentages. The amount you want to raise for product development should be funded by a reduction in operating expenses. Don't cut your pay, profits, or taxes to fund product development. It is clearly an operating expense.

As you watch the product development bank account grow, you can simultaneously begin researching and planning your next product. However, make sure you don’t take your eye off the ball with your first product. As you create more complexity in your business, it’s easy for something to get lost in the shuffle.

As you watch the product development bank account grow, you can simultaneously begin researching and planning your next product. However, make sure you don’t take your eye off the ball with your first product. As you create more complexity in your business, it’s easy for something to get lost in the shuffle.

If you are concerned that it’s taking too long to save up the funds for the second product, this is a red flag telling you that your margins may be slim, and your first product may not be a cash cow. Carefully consider your options in this situation. You may be able to increase prices or cut costs associated with manufacturing or advertising. Or maybe you should cut your losses and not reorder that product as your supply is depleted.

Finally, another common question is, “Can’t I borrow the money so I can scale quicker?” Debt can have a place in business, but often it’s misused. If you haven’t tested out your business model, additional funds may obscure an issue with pricing or sourcing. If those issues exist, then the gross margin may be too low to fund the interest on the loan.

It’s exciting as an entrepreneur to plan and dream about your businesses. Plans and dreams are really where it all starts. By taking the time to consider the financial implications before you expand your brand, you will have a better chance to make those dreams come true.

It may seem counterintuitive, but setting aside your profits does in fact allow you to build your business from a more solid base. It puts Parkinson’s Law on your side to grow organically.

If your profitability isn’t where you’d like it to be, check out my book, Profit First for Ecommerce Sellers.

You can also sign up for the Profit First for Ecommerce Sellers online course.

No Comments Yet

Let us know what you think